Q2 2036 — Is Bitcoin Dead?

Why Bear Markets Are a Feature, Not a Bug

I. Introduction: I’ve Heard This Before

Bitcoin is down sharply from its highs. Headlines ask whether the experiment has finally failed. Strategy just sold 32 BTC. Sentiment is fearful. Leverage has been flushed. The crowd that arrived at the top has left disappointed.

I have seen this movie before. In fact, I wrote about it.

In January 2019, with Bitcoin trading near $3,000 after an 84% collapse from its 2017 peak, I posted a thread arguing something that felt counterintuitive at the time:

“I come to the conclusion that the extreme bull and bear markets of bitcoin are a feature and they speed up the adoption process.”

That thread laid out a simple idea. Bull markets attract capital, developers, and infrastructure. Bear markets do the opposite work. They shake coins out of weak hands and concentrate supply among holders who will not sell. I called them the hodlers of last resort.

Seven years later, the thesis has only strengthened. Every cycle has repeated the pattern. And every cycle, the question returns. Is Bitcoin dead?

The answer is the same as it was at $3,000. No. The volatility is not a disease. It is actually an inevitable feature of accelerating adoption.

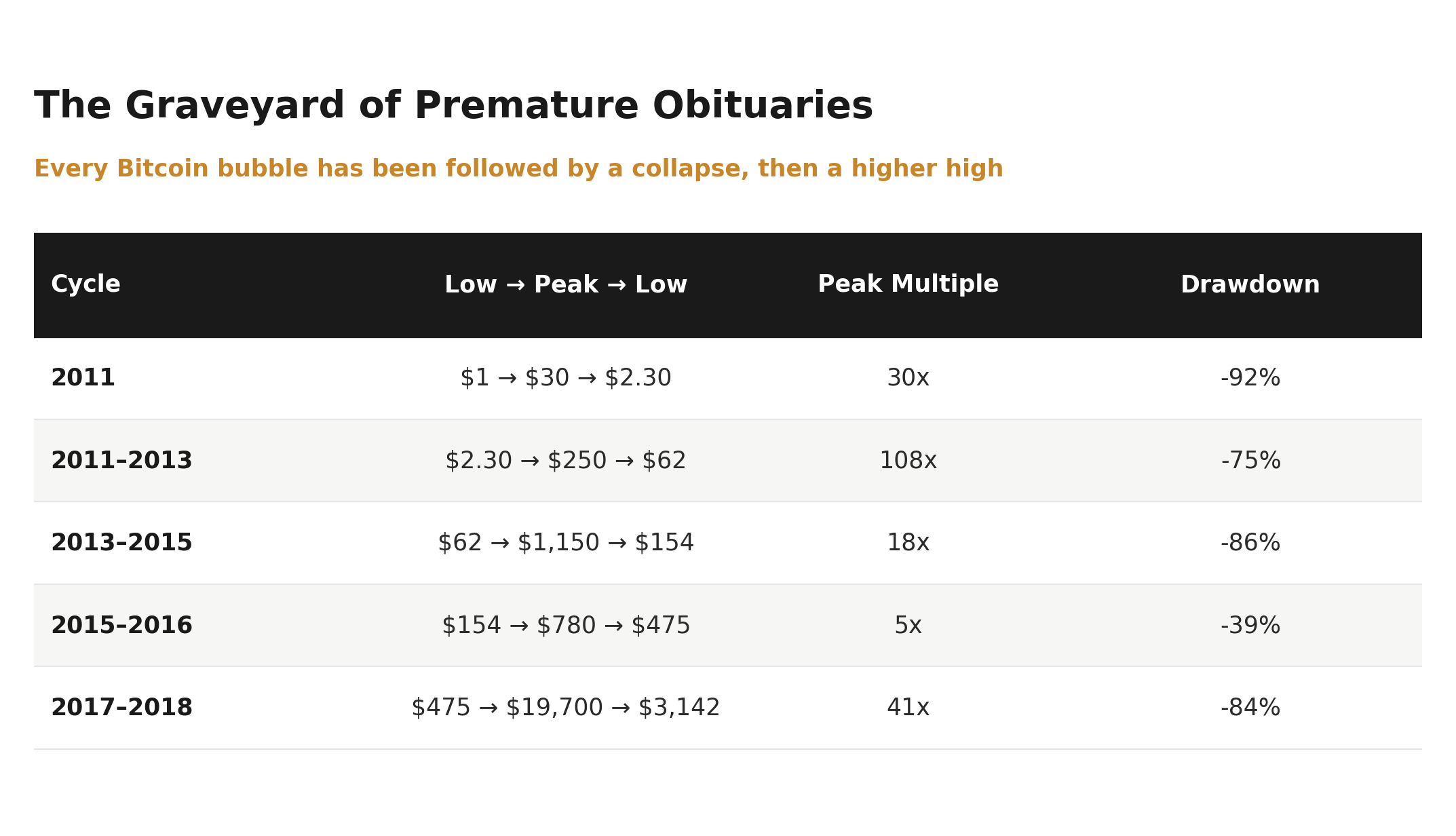

II. The Graveyard of Premature Obituaries

The average person does not know this, but the current drawdown is not the first time Bitcoin has “died.” There have been countless other bubbles, each followed by a collapse severe enough to convince most observers it was over.

The historical record, as I laid it out in 2019, speaks for itself.

Each of these declines produced a wave of obituaries. Each was followed by a new all-time high that dwarfed the prior peak.

The cycles since my original thread have followed the exact same script. That 84% collapse to $3,142, the one that prompted the thread, was followed by a run to $69,000 in 2021. Then Bitcoin fell to roughly $16,000 in 2022, and the obituaries returned in force. From there it ran to $126,000 last year. And now, after another drawdown, we are back near $69,000, with the same question being asked once again.

The pattern is not noise around a trend. The pattern is the trend. Massive advances paired with massive declines are precisely how Bitcoin adoption plays out.

III. How Bear Markets Concentrate Supply

The bull market does the work of expansion. It brings in network effects: developers building infrastructure, institutions allocating capital, and miners.

The bear market does the work of selection. It drives out everyone who never understood what they were holding.

Consider who is forced to sell as the price falls:

The speculators who arrived at the end of the last bubble, bought the top, and never developed conviction. As the price drops, regret turns to capitulation.

The over-leveraged. Margin and liquidations force coins onto the market regardless of the holder’s beliefs. A 50% drawdown becomes a 100% loss for anyone levered.

The miners who must sell production to cover electricity and operating costs, adding steady supply pressure during the decline.

These are the high hands. The weak hands. The hands that should not be holding Bitcoin and do not fully understand it. The bear market peels them off, one liquidation at a time.

And who is left? Who is buying after the price has fallen 70 or 80 percent, after the headlines declare it dead, after their friends have stopped asking about it?

Only the holders with extreme conviction. The ones who can withstand extreme volatility. The ones who understand that Bitcoin’s monetary properties are superior to every alternative and who are not selling anytime soon.

“They have their stash of bitcoin that will never be sold until full adoption and they continue to buy more bitcoin when it seems cheap.” (January 2019)

A bear market is a transfer. It moves coins from the weakest hands to the strongest. The deeper the fall, the more complete the transfer.

This is why I argued in 2019 that price gaps down are not bad for Bitcoin. If a large holder dumped a million coins and the price gapped to a penny, that would be bullish. The hodlers of last resort would absorb a fraction of the entire supply at almost no cost, and those coins would effectively leave the market forever. Every coin absorbed by a strong hand is kindling for the next run.

IV. The Asymmetry: No Market-Based Supply Response

Here is what makes Bitcoin structurally different from every other asset.

In a normal market, rising prices summon new supply. Oil at $120 brings new drilling. Lumber spikes bring new sawmills. Real estate appreciation brings new construction. The new supply caps the upside. Price increases contain the seeds of their own reversal.

Bitcoin has no such release valve.

The issuance schedule is fixed and indifferent to price. Whether Bitcoin trades at $70,000 or $7 million, the network produces the same coins on the same schedule, halving every four years. There is no producer who can ramp output to meet demand. There is no central authority that can dilute the supply.

So when sentiment flips, and it always flips, as the dollar continues to debase and Bitcoin grows more scarce with each halving, the price begins to move up. But the only available supply now sits in the hands of the strongest holders. The very people who held through the entire decline, who bought when it seemed cheapest, who have the least incentive to sell.

The only supply that can come back to market now is psychological. It requires convincing diamond-handed holders to part with coins they spent a bear market accumulating. That is an extraordinarily difficult thing to do.

Demand returns against a wall of unwilling sellers. Price discovers a new range violently. The cycle that “killed” Bitcoin becomes the foundation for the cycle that mints its next all-time high.

“Once the supply finally matches demand, the price will stabilize, weak hands stop selling and the price begins to move up. While demand starts increasing again, the supply remains LOW.” (January 2019)

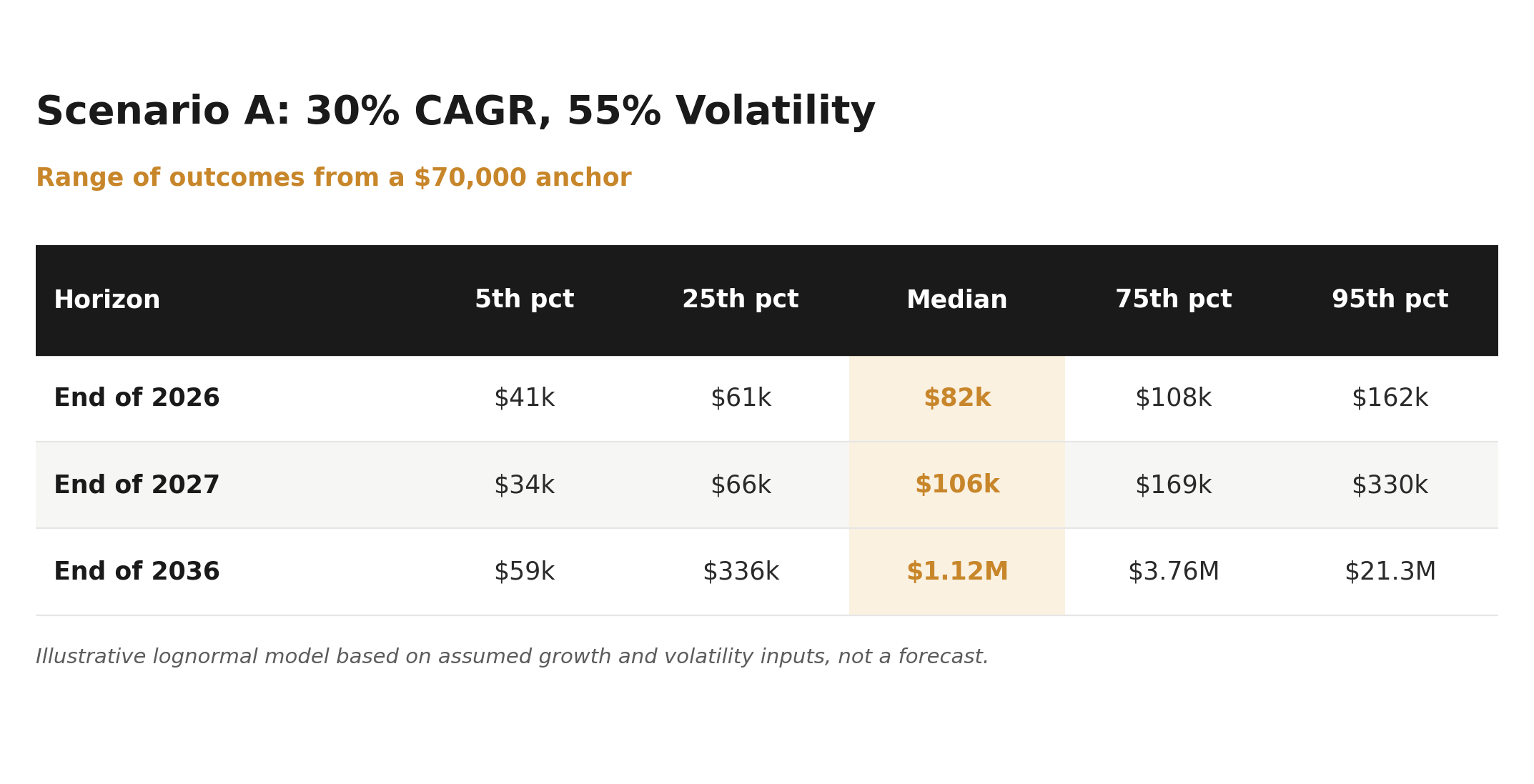

V. The Range of Outcomes

Conviction is not the same as precision. I do not know where Bitcoin trades next quarter, and neither does anyone else. But I can describe the distribution of outcomes that a volatile, high-return asset produces over time.

Assume Bitcoin compounds at a 30% median annual growth rate with 55% annualized volatility. These are modest assumptions relative to its history. Anchoring at $70,000, the lognormal distribution of outcomes looks like this.

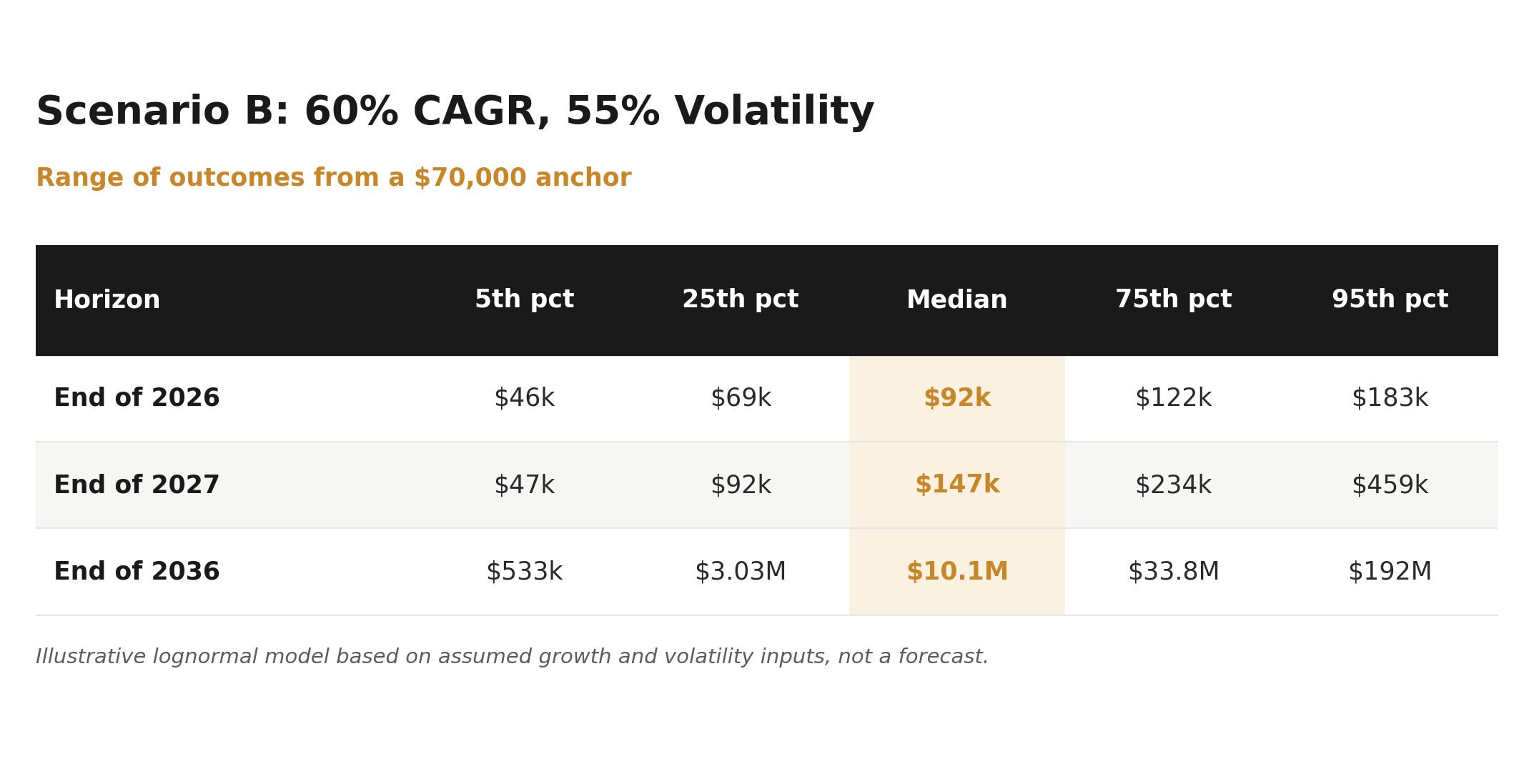

Now raise the growth assumption to a 60% median CAGR, closer to Bitcoin’s realized historical pace, holding volatility at 55%.

Three things stand out.

First, the bear case is survivable. Even at the 5th percentile, a genuinely terrible outcome, 2027 lands near $34k to $47k. Lower than today, but hardly extinction. The asset that “died” is still worth roughly half its current price in the disaster scenario.

Second, the near-term band is wide enough to contain both euphoria and despair. By end of 2026, the same model that puts the median around $82k to $92k also admits a drop into the $40s and a spike into the $160s to $180s. Both the “it’s dead” headline and the “new all-time high” headline live inside one distribution.

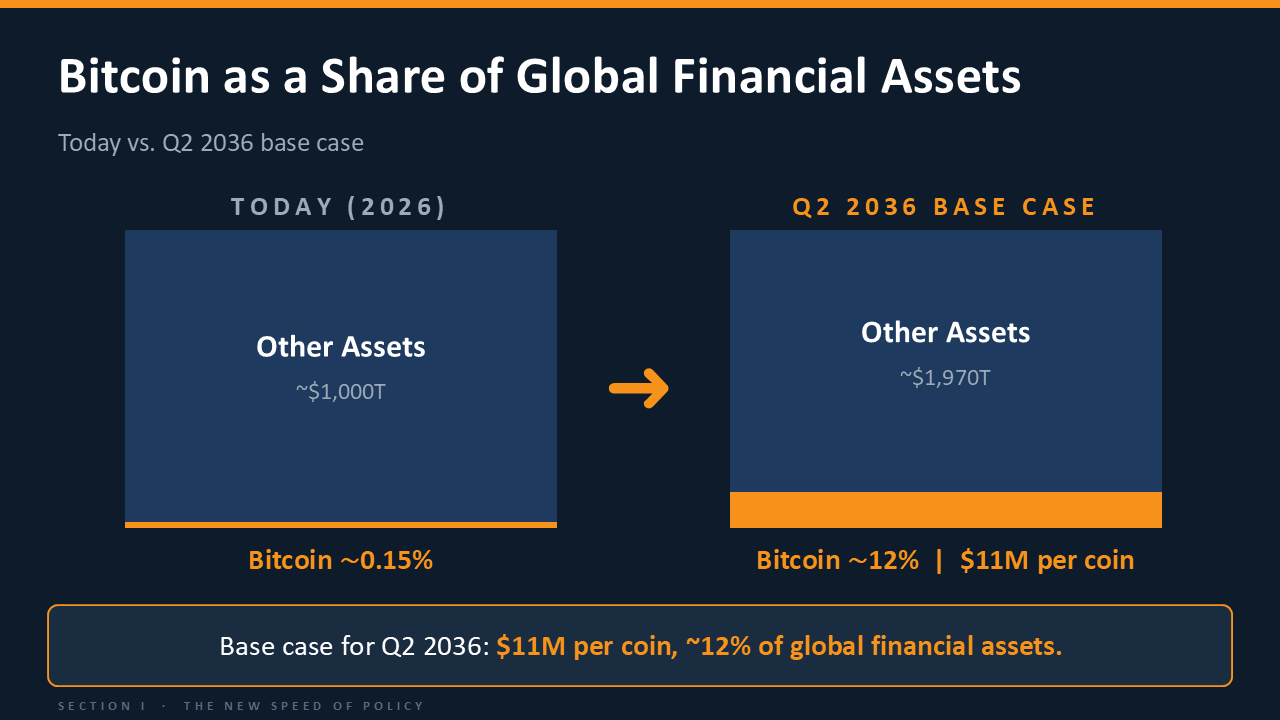

Third, time is the variable that matters. The dispersion explodes with the horizon. At ten years, a 30% CAGR produces a $1.12M median, while a 60% CAGR produces a $10.1M median, squarely on top of the eight-figure thesis I laid out in my previous Q1 2036 letter. The difference between a millionaire outcome and a decamillionaire outcome is not whether you are right about direction. It is the compounding rate, and your ability to still be holding when it resolves.

The volatility that terrifies people on a quarterly basis is the same volatility that produces these terminal ranges. You do not get one without the other. The 50% drawdowns are the toll you pay for the path.

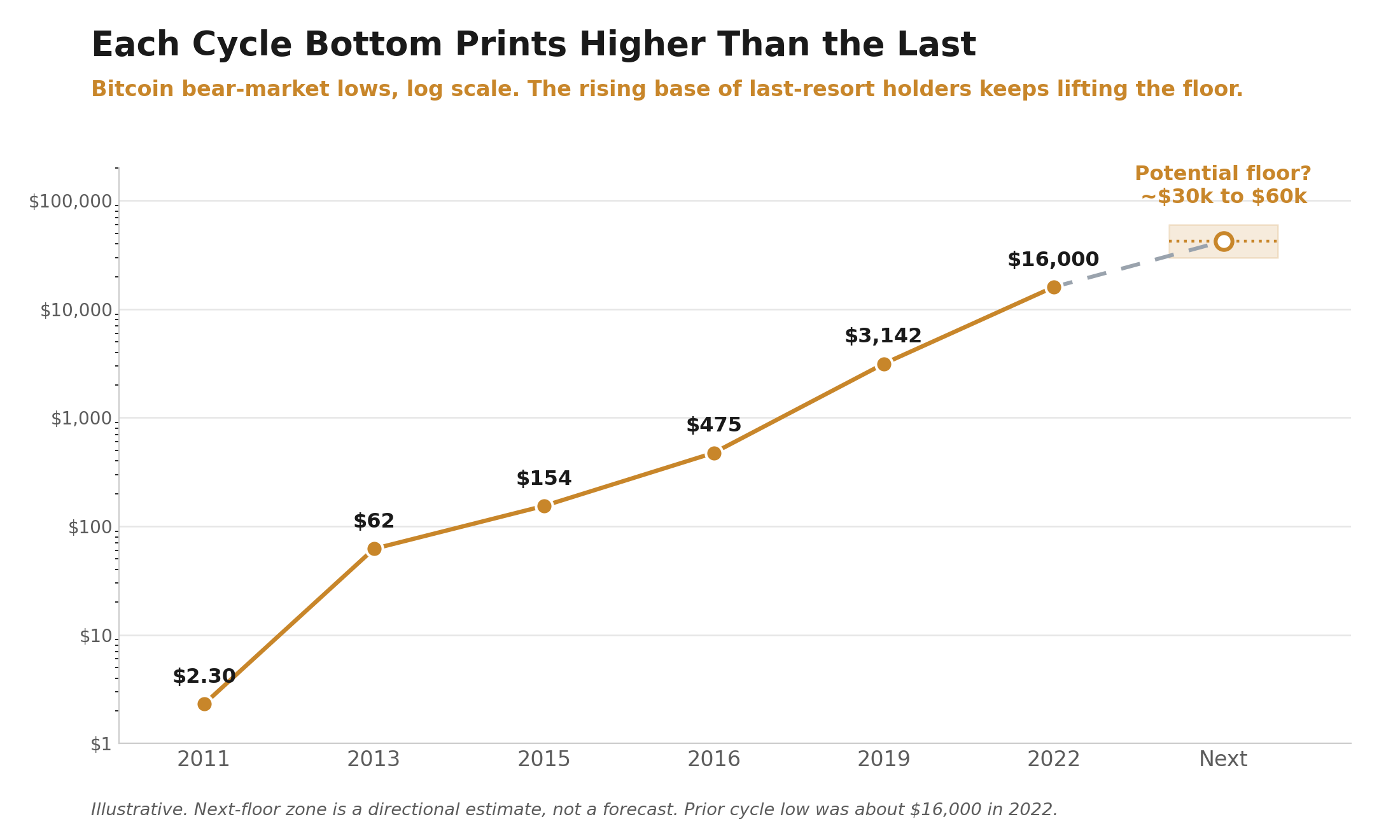

VI. The Base Keeps Rising

There is a way to verify, in real time, that the hodler base is growing rather than shrinking. Each cycle low prints meaningfully higher than the last.

$2.30. $62. $154. $475. $3,142. $16,000. And the next floor, whenever this cycle bottoms, will almost certainly print higher than the one before it.

That rising sequence of lows is the footprint of an expanding base of last-resort holders. Each bear market hands coins to people who will not sell, permanently tightening the float. Each cycle, the pool of patient capital is larger, deeper, and harder to shake out. The supply available to the market keeps shrinking even as the network keeps growing.

This is the cycle that has repeated since 2011, and it will continue until full adoption.

Scarcity produces supply shortages. Shortages produce price increases. Price increases attract attention. Attention drives adoption. Adoption converts speculators into hodlers of last resort. And those hodlers withdraw supply, setting the stage for the next shortage.

The wheel turns again.

VII. So, Is Bitcoin Dead?

No.

Bitcoin is doing exactly what it has always done at this point in the cycle. It is shaking out the people who arrived late, leveraged up, or never understood what they owned, and delivering their coins to the people who did.

The fear you feel reading the obituaries is the process working. The drawdown is not evidence of failure. It is the selection that makes the next advance possible, against a supply that cannot respond.

Seven years ago, at $3,000, I wrote that the extreme bull and bear markets are a feature, and that the further Bitcoin falls, the faster adoption happens. Nothing in the years since has changed my mind. The dollar has continued to debase. The supply has continued to tighten with each halving. The base of last-resort holders has continued to grow.

The people asking whether Bitcoin is dead are, as always, the ones about to hand their coins to the people who know it is not.

See you in Q3.

— Joe Burnett

This letter is for informational purposes only and should not be considered financial, investment, or legal advice. Opinions expressed are my own and do not constitute recommendations. Always conduct your own research before making financial decisions.

Projection ranges are illustrative lognormal models based on assumed growth and volatility inputs, not forecasts. Actual outcomes may differ materially. Current Bitcoin price reference of roughly $68,900 as of June 2, 2026, per Perplexity Finance. $70,000 used as a round anchor.

Great article - appreciate your insights and research.

One lingering question that pops into my head when price fluctuates this much is: if bitcoin is this volatile how can it still be considered “money”? If I have an emergency and need to pay a medical bill, and have to sell bitcoin to cover the bill (because I have no cash!), that’s a really difficult pill to swallow. What’s the mindset solution to this dilemma? Thanks!

Strong article, Joe.

I'd be curious to hear more about what you meant here:

"If a large holder dumped a million coins and the price gapped to a penny, that would be bullish."

You must not be talking about the USD price dropping to $0.01, right? There would be no recovery from there.