Q2 2035 — The Valuation Reset

How the decline of stock and real estate valuations will unlock a global wealth renaissance—driven by bitcoin and accelerated by bitcoin treasury companies.

I. Introduction: The Coming Reset

Over the next 10 years, stocks and real estate will crash, and everyone will be better off. It sounds crazy, right? Why would anyone want the stock market to crash? Most people have their wealth tied up in stocks—of course they want stock prices to go up.

But what if high stock prices aren’t actually good for individuals or society as a whole? What if lower valuations—yes, even a crashing stock market—are actually better for everyone in the long run?

Now, let me be clear: I do not think U.S. stocks are about to crash in dollar terms. In fact, by design, I believe stocks will continue rising indefinitely when measured in dollars. Why? The dollar is designed to debase against basic consumer goods, so anything just as scarce, or especially anything more scarce than basic consumer goods will continue to go up when measured in dollars.

But this creates an issue. Anything slightly more scarce than dollars gets hoarded, as everyone knows they cannot hold dollars long term. This has led to the valuations of stocks and real estate getting bid to historically high levels, as investors buy these assets to avoid holding dollars. In other words, the multiples people pay for stocks—like price-to-earnings (P/E) ratios—are currently unsustainably high.

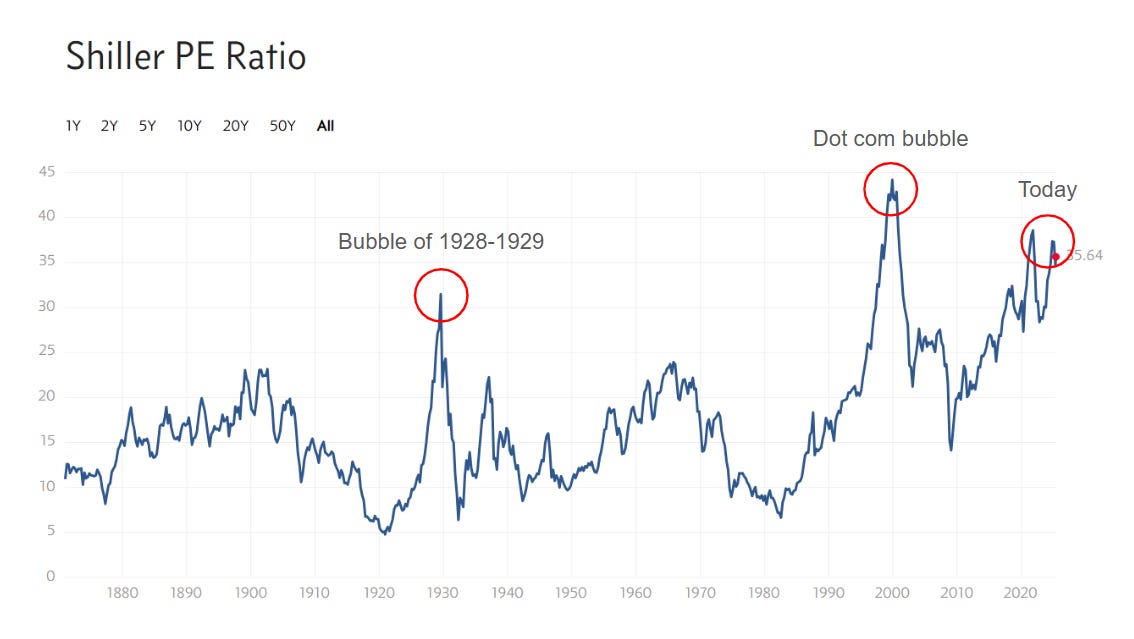

As of May 2025, the Shiller CAPE ratio stands at 35.64, significantly above its historical mean of 17.24 and median of 16.04.1

II. Why High Valuations Hurt Everyone

A valuation collapse—where investors demand higher returns before deploying capital—would be a good thing for both individuals and society as a whole. This shift is coming because the world is upgrading to bitcoin as money, which enforces a dramatically higher hurdle rate for investments.

Now instead of ensuring you're growing the amount of dollars you have, which is easy because dollars are debased over time, you must ensure you’re growing the amount of bitcoin you have, which is difficult because bitcoin becomes more scarce over time.

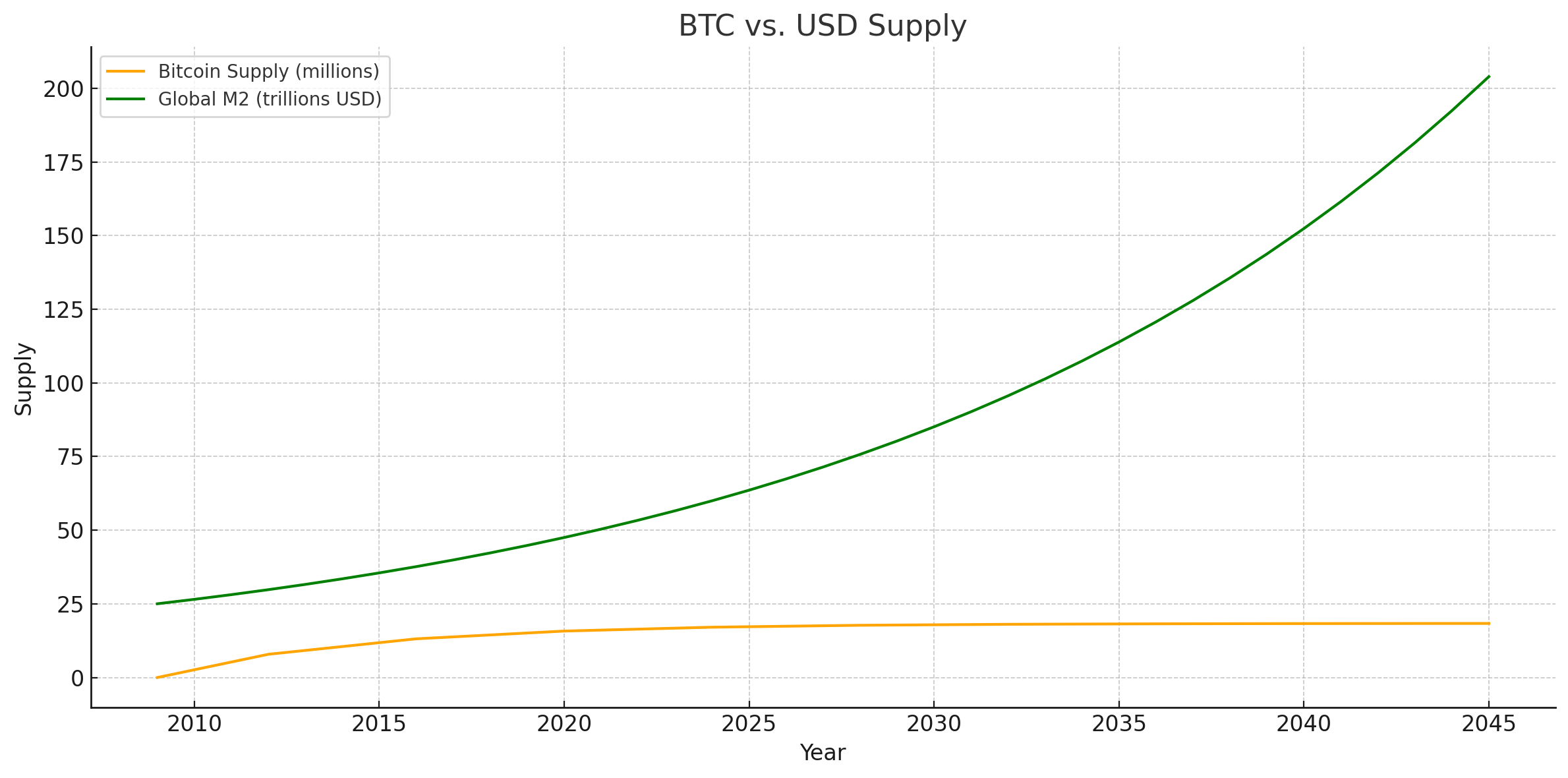

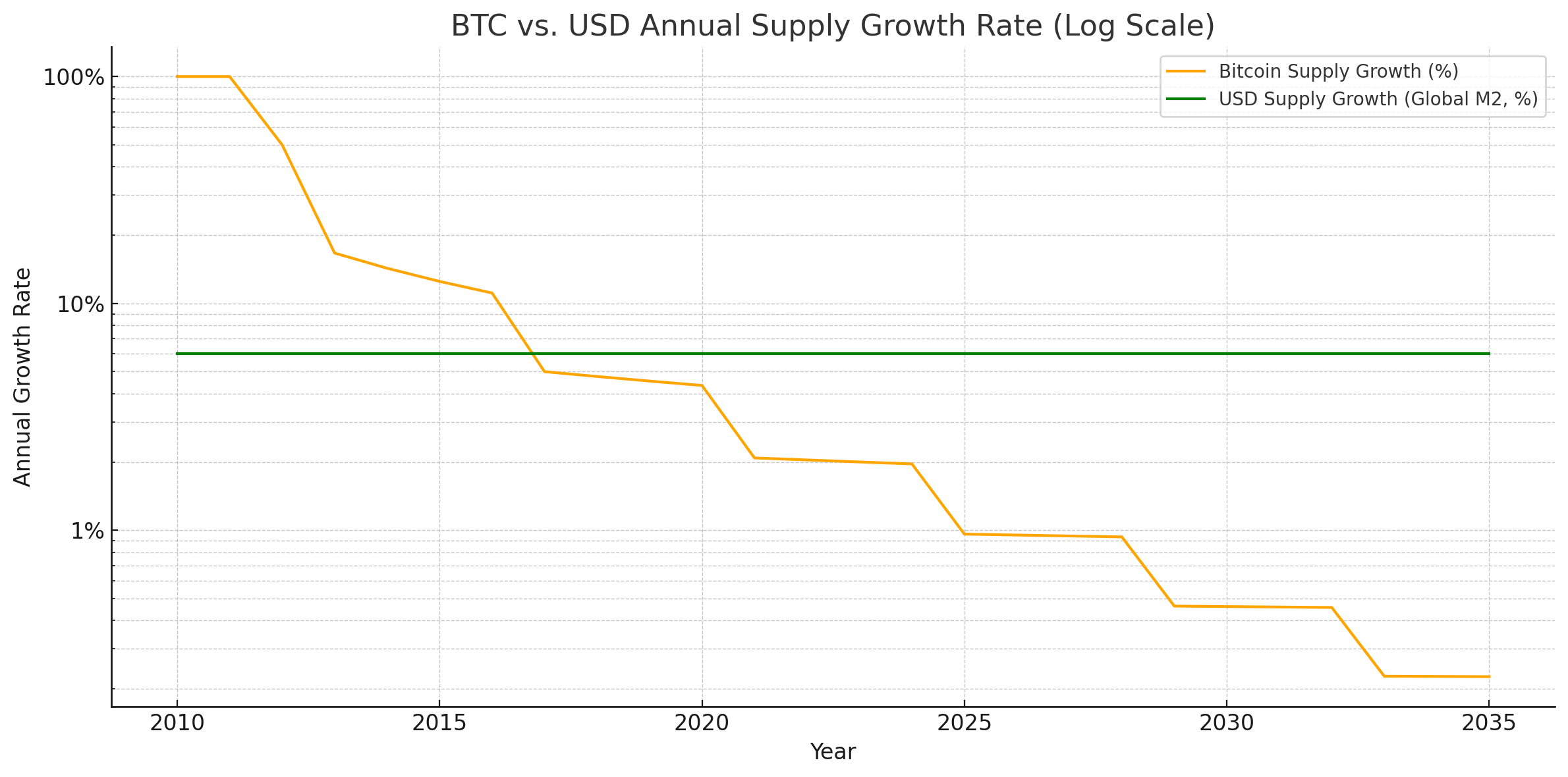

As of 2025, bitcoin’s supply is growing less than 1% per year—forever capped at 21 million. Meanwhile, the global USD supply is compounding at ~8% annually.

By 2035, bitcoin’s annual supply growth rate will fall below 0.2%. The supply of dollars will be growing at a ~40x faster rate.

This monetary transformation will rewire how capital is allocated, moving away from speculative bubbles and toward real, productive businesses.

At first, this idea of a stock and real estate collapse being good for humanity may seem counterintuitive. We’re conditioned to believe that rising stock prices equal economic strength and prosperity. But the reality is, when money is broken, valuations become too high, capital allocation gets distorted, real growth slows, and it becomes more difficult for individuals, businesses, and society as a whole to generate meaningful returns.

The Individual Perspective: Buying Future Earnings

When you buy a stock, you’re not just buying a ticker symbol—you’re buying future earnings. That’s the entire point of investing, and the more you pay for those future earnings, the worse your return.

Let’s break it down with an extreme example:

High valuation (P/E of 50): You pay $50 for $1 of annual earnings. It takes 50 years to fully recoup your investment, assuming no change in earnings.

Low valuation (P/E of 1): You pay $1 for $1 of annual earnings. You fully recoup your investment in just one year.

Holding all things equal, you’d rather buy the same company at a lower valuation over a higher valuation. Just like you’d rather buy the same cup of coffee for $1 instead of $50. Lower valuations mean investors get their money back faster through future earnings, instead of relying on someone else paying a higher price later. Today, with the Shiller PE ratio at 35, investors are paying $35 for every $1 of annual earnings. Unless profits grow dramatically, it will take decades to recoup that investment.

The Societal Perspective: Consequences of a Broken Hurdle Rate

At a macro level, high valuations don’t just hurt individual investors—they distort the entire economy. If capital is allocated based on anything that beats a very low hurdle rate, rather than real profitability, it creates massive inefficiencies.

This is exactly what’s been happening for years. Broken money has encouraged investors to:

Pour money into zombie companies that never generate real profits.

Speculate wildly on meme stocks and crypto tokens.

Drive real estate prices to absurd, unlivable levels, making housing unaffordable for new families.

Keep funding businesses that survive on low interest rates rather than actual demand.

Perpetually buy the largest 500 companies in the United States at any valuation making it accretive for mega corporations to acquire smaller companies extensively and pursue growth recklessly.

When interest rates are low, the hurdle rate for investing is also low. In fact, research from the Bank for International Settlements shows that the share of zombie companies—those unable to cover interest payments from profits—has surged from around 2% in the late 1980s to over 12% in recent years.2

Rather than investing in innovation or capital expansion, many firms used cheap borrowing to buy back their own stock—boosting earnings per share while taking on debt. JPMorgan found that nearly 30% of buybacks during the 2016–2017 period were debt-financed.3 Central banks like the IMF and BIS have warned that prolonged periods of low real interest rates lead to excessive risk-taking. Investors flood into anything offering even the illusion of returns—from meme stocks and junk debt to crypto tokens and SPACs—because the opportunity cost of holding cash is so high.4

Investors don’t need to be selective—they just need to avoid holding dollars. That’s why we see a flood of capital into low-quality projects and overpriced assets that don’t actually produce meaningful value.

III. The Solution: Sound Money, A High Hurdle Rate, and Lower Valuations

A higher hurdle rate forces investors to demand stronger returns, which changes everything:

Investors become more selective. Money flows into businesses that generate real profits instead of propping up weak, unprofitable companies.

Capital returns faster. Investors don’t have to wait decades to recoup their investment—they get paid back sooner through earnings.

Fewer speculative bubbles. No more throwing money at meme stocks, zombie firms, crypto tokens, or overpriced real estate just because “prices always go up.”

A high hurdle rate forces only the best investments to be pursued. It raises the bar for what qualifies as a good use of capital. Instead of thousands of people pouring money into a bunch of half-baked, mediocre ideas (the modern diversified portfolio), we get a world where capital is allocated to truly excellent, highly productive projects.

Bitcoin: The High Hurdle Rate

This is where bitcoin will transform the entire global financial system. Unlike the dollar, which is constantly debased, bitcoin provides a fixed, unchanging unit of account. It creates a high hurdle rate because the opportunity cost is clear—if an investment doesn’t outperform bitcoin, it’s simply a bad investment.

If an investment turns 1 bitcoin into 0.99 bitcoin, it's a failure.

If it turns 100 bitcoin into 99 bitcoin, it's a failure.

Investors are forced to ask: Is this project truly worth risking my bitcoin?

This radically reshapes how capital is allocated. In a bitcoin-denominated world, there’s no incentive to throw money at nonsense. Investors won’t just buy every asset that exists today. They’ll hold bitcoin until they find an investment that’s actually worth deploying capital into.

IV. The Future: More Productive Investments, Less Waste, More Wealth

Right now, we live in a world where money is easy to access—if you already have a stockpile of assets or you're part of the right network. Capital is concentrated in the hands of those closest to the money printer: governments running multi-trillion-dollar deficits and the ultra-wealthy who have privileged access to cheap loans through the banking system. These groups don’t need to justify high returns; they just need to beat the artificially low hurdle rate set by central bank monetary policy. As a result, capital gets funneled into semi-good investments—projects that may not be outright failures, but also aren’t the best possible use of resources.

When the hurdle rate is drastically increased—when every investment must outperform bitcoin—this changes everything.

Projects that don’t generate strong, real returns will no longer attract capital. And that’s not a bad thing—it’s a great thing. The factories, tools, software, hardware, real estate, and labor that would have gone into semi-good projects still exist. But instead of being locked up in low-efficiency businesses or speculative bubbles, that capital will be utilized for exceptional opportunities.

In a bitcoin-denominated system, capital will only be deployed when the expected returns are extraordinarily high—because investors and entrepreneurs won’t settle for less. Only those with the absolute best use for resources will deploy them. The bar will be so high that only the most efficient, high-impact projects—those capable of truly outperforming bitcoin—will get funded.

This means:

No more wasting resources on barely profitable zombie companies propped up by cheap debt.

No more funneling trillions into speculative nonsense simply because interest rates are low.

No more economic stagnation driven by misallocated capital.

Instead, we’ll see an explosion of real innovation. Capital will flow toward high-impact, high-efficiency businesses that create real value. The economy will become orders of magnitude more productive, leading to an era of unprecedented economic progress—one where resources are allocated with maximum efficiency.

Individuals and businesses won’t perpetually need to invest or build a diversified portfolio. Instead they can simply save bitcoin and only invest when they find a very good opportunity.

This means society as a whole will still have all real estate and profitable businesses that exist today, but now we will also have a massive ever growing pile of savings (bitcoin) that could potentially be worth more than all stocks and real estate combined, as individuals no longer need to mindlessly buy stocks and real estate to save for the future.

This shift is already evident as investors are beginning to favor bitcoin over traditional assets for long term savings. In 2024, BlackRock's iShares Bitcoin Trust (IBIT) attracted over $37 billion in net inflows, making it the most successful ETF launch in history.5 Additionally, firms like Unchained help secure over $10 billion in bitcoin for individuals, family offices, and both private and public companies.6 Last, companies like Semler Scientific (NASDAQ: SMLR) are leading the corporate adoption of bitcoin as a treasury reserve asset by issuing low interest rate (4.25%) unsecured convertible debt to buy bitcoin, with no short-term repayment risk or liquidation risk.7 It’s a contrarian and intelligent strategy to amplify the future returns of bitcoin—one that perfectly aligns with my conviction, which is why I’m joining Semler as Director of Bitcoin Strategy.

V. Toward a Wealthier, More Productive World

A crashing stock market, or more specifically, a significant reset in valuations, is not the catastrophe people assume. It’s actually healthy. Lower valuations allow individuals to buy future earnings at better prices, and they force society to allocate capital into highly productive businesses instead of speculative nonsense.

Bitcoin enforces this shift by setting a high hurdle rate—one that discourages wasteful investments and encourages real, productive growth. In the long run, this is how we transition from an economy built on speculation to an economy built on actual value creation. It’s time to reprice the economy in bitcoin.

See you in Q3.

— Joe Burnett

This letter is for informational purposes only and should not be considered financial, investment, or legal advice. Opinions expressed are my own and do not constitute recommendations. Always conduct your own research before making financial decisions.

Great post Joe :)

Well said Joe! Looking forward to the monetary premium deflation.